In an effort to attract and retain talent, many companies have historically chosen to offer their employees financial contributions towards private health insurance plans. While this benefit may seem appealing at first glance, it can inadvertently lead to missed opportunities for better health outcomes among the workforce for several reasons:

1. Inflexible and Restrictive Coverage

One of the key drawbacks of private health insurance plans is their inflexibility and restrictive nature. The base plans offered as part of an employment package typically exclude coverage for most services aside from the basic services, likely due to their cost-efficacy for the private health insurer. This can leave employees vulnerable to out-of-pocket expenses for important medical services left out of the plan and create a financial barrier to accessing necessary treatments and preventive care.

Moreover, most insurance providers restrict coverage for pre-existing conditions on these base plans, limiting employees’ ability to address ongoing health issues effectively – especially when they’re existing concerns. A survey conducted by the Commonwealth Fund in 2019 revealed that 35% of privately insured adults in the United States reported difficulty in paying medical bills due to their plan’s restrictions.

2. Stand Down Periods and Delayed Access to Care

Private health insurance plans often come with stand-down periods, during which employees are required to cover the costs of specific services personally until they become eligible for coverage. These waiting periods can last several years, especially for ‘in demand’ and highly accessed services, which may force your employees to delay accessing certain healthcare services, especially if they don’t have additional private funds in amongst our high cost of living and soaring mortgage rates.

Long stand-down periods on private health insurance plans can lead to negative health outcomes by significantly delaying essential healthcare access. During these waiting periods, individuals are required to cover the costs of specific services out-of-pocket until they become eligible for coverage. As a result, patients may postpone seeking necessary medical attention, preventive care, or treatments, allowing health conditions to worsen over time.

For example, someone experiencing concerning symptoms may delay visiting a specialist or undergoing diagnostic tests due to the financial burden. This delay in care can lead to missed opportunities for early diagnosis and timely treatment, potentially resulting in the progression of illnesses and reduced chances of successful recovery. Ultimately, long stand-down periods hinder proactive healthcare and preventive measures, contributing to negative health outcomes for those insured under such plans.

3. Focus on Reactive Instead of Proactive Healthcare

The basic plan coverage that is typically included in employer private health insurance schemes largely focuses on ‘reactive’ healthcare. This means that employees are often covered for medical treatments and services once they are already ill, rather than prioritising preventive care and early intervention, with a study published in the Journal of General Internal Medicine finding that individuals with private health insurance were less likely to receive preventive services compared to those with other types of insurance.

By neglecting proactive and preventative services, such as regular health screenings and wellness check-ups, these insurance plans fail to catch health issues in their early stages when they are more manageable and less costly to treat. Early detection allows for timely interventions, lifestyle adjustments, and necessary medical care to prevent or minimise the progression of diseases. Without these proactive measures, individuals may unknowingly harbour underlying health conditions that could have been addressed, leading to missed opportunities for better health outcomes and potentially allowing manageable conditions to escalate into more severe health challenges.

4. Insufficient Coverage and High Out-of-Pocket Costs

While private health insurance plans may cover a percentage of medical expenses that are approved under the specified plan, the remaining out-of-pocket costs can still feel substantial in today’s financial climate, especially with missed mortgage payments looming. This financial burden can dissuade employees from seeking necessary medical care, leading to potentially severe health consequences in the long run. This can also make private health insurance feel ‘not worth it’, especially if employees are only making one or two claims per year and having to pay the monthly top-up fees, plus the out-of-pocket percentage of the bill.

5. Limited Focus on Comprehensive Family Health

Private health insurance plans also exclusively revolve around the individual employee, neglecting to recognise the extent to which one person’s health is impacted by the health of their immediate family. By offering a private health insurance plan that fails to address the health needs of employees’ families, employers miss an opportunity to foster a healthy and supportive environment for their workforce by providing an alternative solution.

Research published in the Journal of Occupational and Environmental Medicine suggests that employees with supportive family environments are more likely to engage in healthier behaviours and experience improved overall health. By not considering the well-being of employees’ families, employer-sponsored private health insurance plans may inadvertently hinder the potential for positive health outcomes among the entire household.

The Solution: Switching From Private Health Contributions To Employer Aid Payments

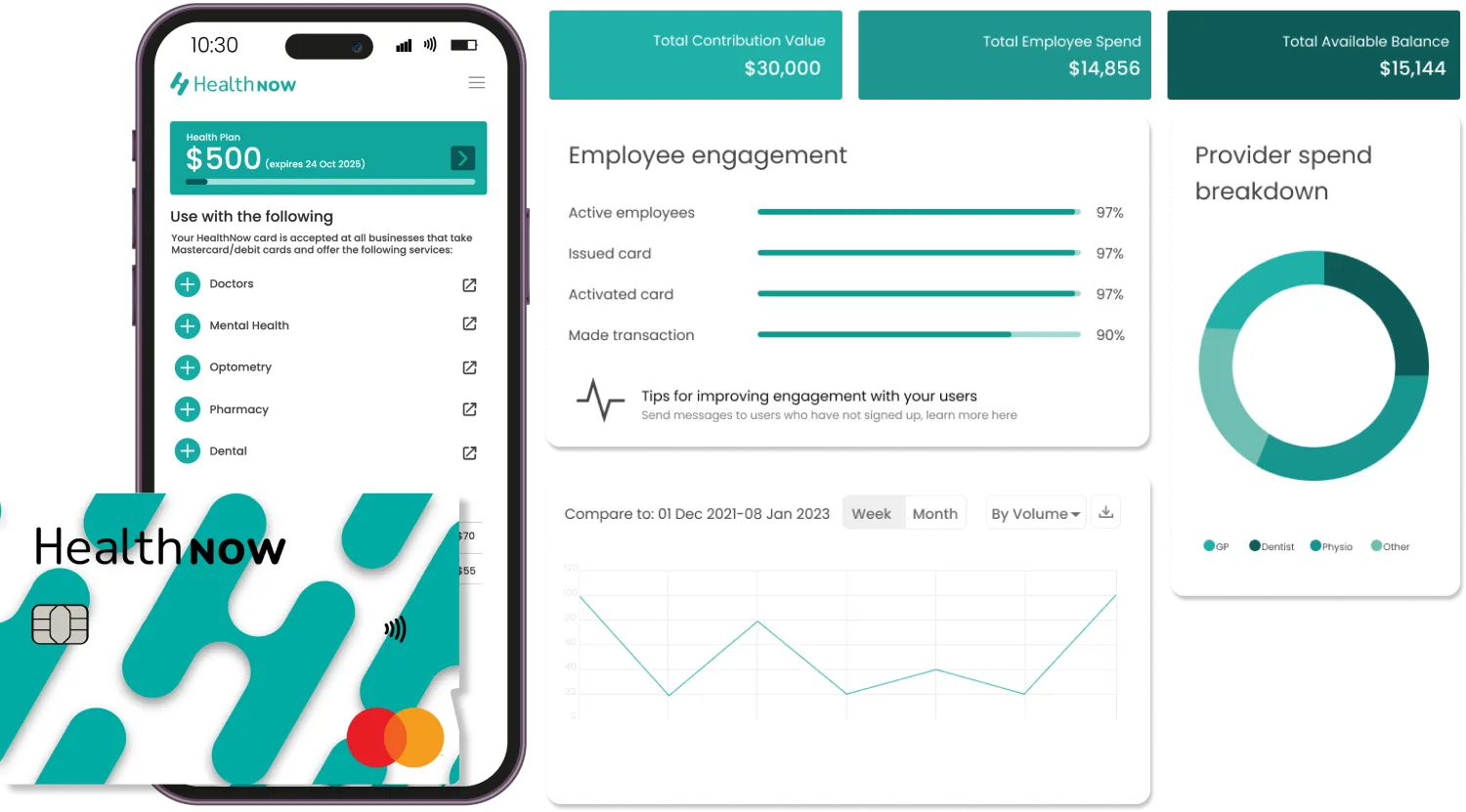

Employer aid is a recognised proactive health approach that differs from private health insurance in each of the categories that we’ve listed above. Employer aid is a specified financial contribution that is delivered as a payment to an employee’s dedicated health account via the HealthNow app, which can only be used on health and medical-related services and products. This includes proactive health care such as seeing a nutritionist to get on top of nutrition or seeing a physiotherapist at the first sign of musculoskeletal pain, as opposed to when it has worsened to the extent that a person physically cannot come into work or perform their work duties.

The quantity of the funds is chosen by the employer, and is available for employees to use throughout the year in much the same way they use a digital card on their phone, working at any eftpos terminal where Mastercard is accepted. Employees have control over which health services to spend their funds on within the health service categories approved by the employer, and available within HealthNow’s service suite. Businesses are not charged for any funds that are unused by their employees at the end of their annual period. In some cases, employers may also choose to extend the use of the funds to the family members of the employee – this remains at the full discretion of the employer.

Operating across New Zealand and the US, HealthNow makes offering employer aid easy and simple by welcoming you into their AI-driven platform and international technology that delivers a custom solution to your business – HealthNow designs your employer aid based on your needs and requirements. The onboarding process for employer aid is free and easy, and you receive impact statements that give you a breakdown of how the funds are being spent, to best help you direct health initiatives in the future.